A few early adopters of the 401(k) plan design for retirement savings recently told the Wall Street Journal that the platform was always intended to be a supplement to traditional defined benefit pension programs and social security. Instead, the tax-deferred 401(k) savings plan has replaced pensions almost entirely in an effort by employers to reduce the increasing risk, cost and regulation associated with maintaining a defined benefit pension plan.

In other words, the 401(k) was never intended to be a retirement plan but a savings plan. Because money saved for retirement is not automatically annuitized when the time comes, retirees must somehow manage their extremely volatile longevity risk, requiring them to decide how much to spend each year without having any indication of how long they need their money to last. With that in mind, there is a growing consensus among retirement industry experts that guaranteed income in the form of annuities needs to be part of the retirement equation.

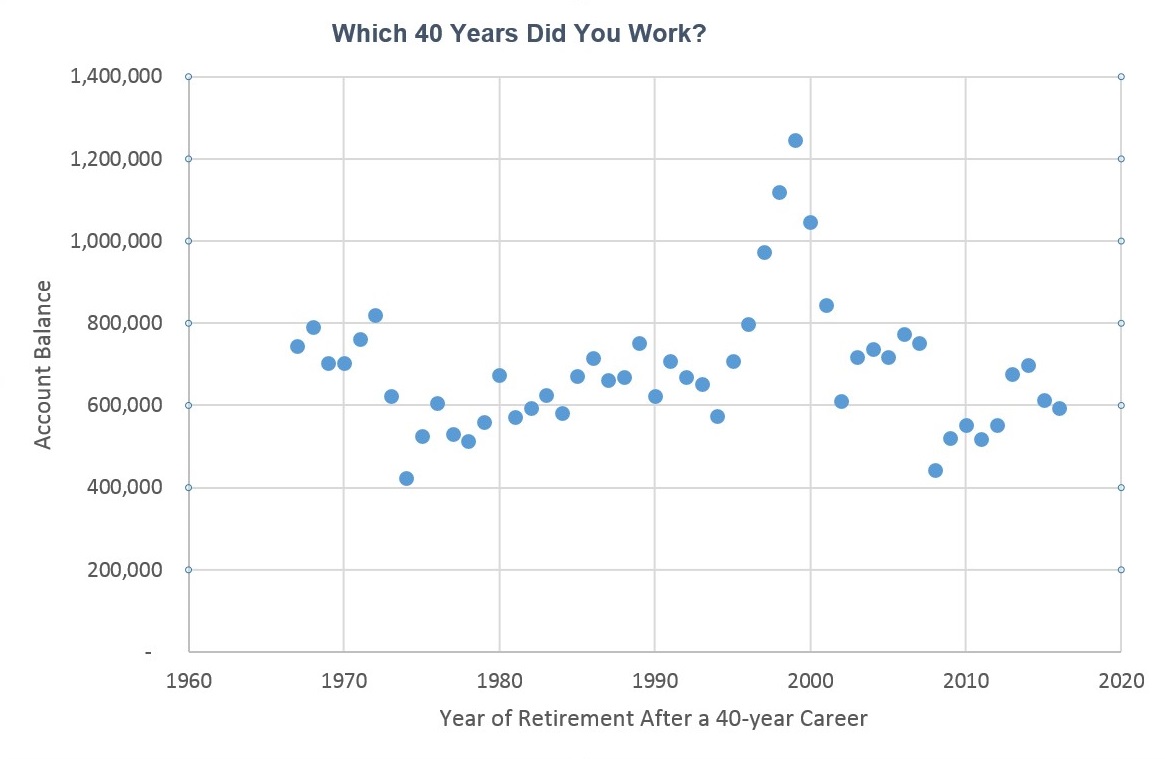

To illustrate how unstable retirement benefits can be with a defined contribution strategy such as a 401(k) plan, the chart below defines the expected balance that an employee would have with annual deposits of $1,000 over a 40-year career. For simplicity, we assume that 100 percent of the money is invested in an S&P Index fund for the entire period.

First, we should take a pause and bask in the glory of compound interest. If an employee contributed only $1,000 per year, even the worst 40-year period in history would provide an account balance of $423,000. However, this pales in comparison to the $1.25 million that this employee would have received had he or she been fortunate enough to retire in 1999. This brings us to the point of this illustration: two people could have identical contributions for the same duration with identical long-term investment strategies, with one person receiving three times the benefit as the other due entirely to the dumb luck of the year they were born.

This multiple can exceed 20 times or more when we factor in the myriad ways people can enter and exit the equity market, which is very often poorly timed. The final amount of employer provided income is chaotic and unpredictable, which brings us to a very unsettling truth about the billions of dollars that employers have poured into 401(k) plans over the years:

Employers have no idea how much retirement income they have provided for any 401(k) plan participant.

The most effective retirement savings plans balance risk and cost along three legs of a stool: social security, pensions and savings. The ideal plan embraces the desired elements of a defined benefit plan without the risk and cost to the plan sponsor that drove them away from defined benefit plans in the first place.

Fortunately, there is a way to deliver such a benefit: create a new, stand-alone, qualified defined contribution plan that consists solely of employer contributions, which are used to purchase deferred annuities during the employee’s working life.

This 401(a) type plan would be structured as a profit sharing plan with the following design features:

- Employer makes contributions to the plan on behalf of each employee, which can vary based on salary, position, years of service, etc.

- Each contribution purchases a piece of deferred annuity based on the age of the participant.

- Upon separation of service, the participant receives an annuity certificate for their accrued benefit payable at the plan’s retirement age.

- There are no other distribution options, other than at death.

By channeling a portion of the current 401(k) match into this new plan, employers would be reinstating that missing third leg of the stool and delivering affordable, equitable and more secure retirement benefits to their participants. Moreover, employers will once again know exactly how much retirement income they are providing for their employees.

Jack Abraham is a principal at professional services firm PwC. Matthew Kasper is a retirement director at the firm. To comment, email editor@talenteconomy.io.